File MTD quarterly updates on the go from your mobile

FreeAgent’s making it easier to stay on top of Making Tax Digital for Income Tax admin.

Here's how to stay on top of your finances - and keep HMRC happy - when selling online.

FreeAgent’s making it easier to stay on top of Making Tax Digital for Income Tax admin.

Building FreeAgent for Landlords - a product tailored to make accounting for rental income as simple ...

In the meantime, feel free to browse for more handy content and useful ideas.

Transform messy letting agent statements into structured, categorised and reconciled entries. Automat...

Manage your property finances and get Making Tax Digital for Income Tax done with FreeAgent for Landl...

Sending your first quarterly update for Making Tax Digital for Income Tax? Here’s what you need to know.

Find out the consequences of missing an MTD deadline in the first year - and how to avoid a fine.

Find more hours in your day with these time-saving hacks from FreeAgent’s support accountants.

FreeAgent's Director of product says building better bookkeeping's our keystone for simplifying CIS.

Automate MTD tasks and manage quarterly client compliance more efficiently at scale.

Making Tax Digital is coming. These tips will help you get it done.

Calling all keen beans: get ahead of the game and file your tax return early.

Consumer champion Dom Littlewood talks to sole traders affected by Making Tax Digital for Income Tax.

FreeAgent’s Director of Product looks beyond the MTD deadline and shares how practices' operational r...

FreeAgent now allows you to manage CIS income directly from bank data, reducing manual admin for prac...

New legislation will give the UK the toughest laws on late payments in the G7, says the government.

Navigate the changes to minimum wages, business rates and Making Tax Digital.

From catching tax mistakes to demystifying VAT, these small businesses explain why their accountants ...

Urban legends aren’t going to help you prepare for Making Tax Digital for Income Tax, but we can.

While the Chancellor made no policy announcements, April will still see changes for small businesses.

FreeAgent's Director of Product shares our plans and goals for a transformative year.

This is what Making Tax Digital will actually look like for sole traders and landlords.

Here’s how to lead tough conversations and transition your clients to a digital-first world with conf...

Improving long-term visibility into cashflow is a step towards more confident decisions. Here are thr...

If you sell on eBay, Vinted or Etsy, when do you have to start paying tax?

What does the first year of MTD for Income Tax have in store for practices? We’ve pulled together all...

If you’ve been contacted about Making Tax Digital - don’t panic! Here’s what you need to do.

We’re excited to announce that FreeAgent now integrates with Fathom. This new integration helps busin...

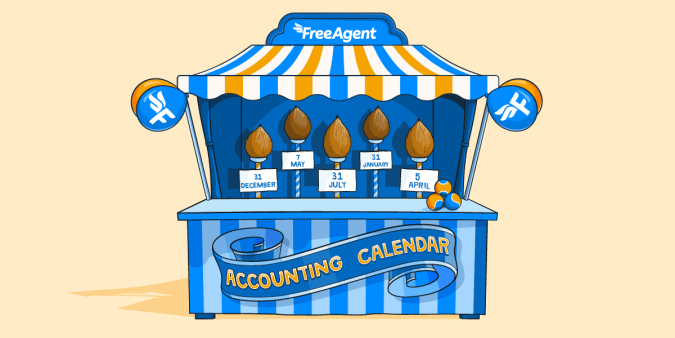

Roll up, roll up! It’s time to get this year’s important tax deadlines in the diary with our free dow...

Here are the numbers you need to plan for a profitable 2026.