How to complete a Self Assessment tax return

Once you’ve registered for Self Assessment, you can complete your Self Assessment tax return and file it to HMRC. In order to do this, you’ll need to provide HMRC with information that will differ depending on your circumstances, and whether you’re a sole trader, limited company director or a partner in a partnership.

In this guide, we’ll help you understand which sections of the tax return you’ll need to complete and what information you’ll need to provide.

Getting started

In order to complete your Self Assessment tax return, you’ll need to have various pieces of information to hand, including:

- your Government Gateway user ID

- your National Insurance number

- your UTR number

- relevant financial records such as details of your income, expenses and any pensions or taxable state benefits you received during the tax year in question

You can check out our dedicated guide to make sure you have everything you need in order to fill in your tax return.

Your Self Assessment tax return includes a Main Return (SA100) and a number of additional sections that HMRC calls ‘supplementary pages’.

The sections that make up a Self Assessment tax return are summarised in the table below. Everyone who files a tax return must complete the Main Return, but the supplementary pages you will need to complete will depend on your circumstances:

| Section | Who needs to fill in this section? |

|---|---|

| Main Return (SA100) | The main section of the Self Assessment tax return. Everyone who files a tax return must fill in this section. |

| Additional information (SA101) | You may need to fill in the ‘Additional information’ page(s) if you received less common kinds of income during the tax year in question, and if you are entitled to certain tax reliefs. |

| Employment (SA102) | You may have to fill in the ‘Employment’ page(s) if you were an employee, director, office holder or agency worker during the tax year in question. |

| Self-employment (SA103) | You may have to fill in the ‘Self-employment’ page(s) if you worked for yourself as a sole trader during the tax year in question. |

| Partnership (SA104) | Each partner in a partnership must fill in the ‘Partnership’ page(s) on their Self Assessment Tax return. One partner will also have to complete a separate Partnership Tax Return (SA800). |

| UK property (SA105) | You may have to fill in the ‘UK property’ page(s) if you received income from UK property during the tax year in question. |

| Foreign (SA106) | You may have to fill in the ‘Foreign’ page(s) if you were entitled to foreign income over certain levels during the tax year in question. You may also have to complete it if you received income from a person abroad by transfer of assets during that tax year, or if you want to claim relief for foreign tax paid. |

| Trusts etc (SA107) | You may need to fill in the ‘Trusts etc’ page(s) if you received (or are treated as having received) income from a trust, settlement or the residue of a deceased person’s estate during the tax year in question. |

| Capital Gains summary (SA108) | You may need to fill in the ‘Capital Gains summary’ page(s) if you made any chargeable gains by selling certain assets, including stocks or shares, land and property or a business, during the tax year in question. |

| Residence, remittance basis etc (SA109) | You may need to fill in the ‘Residence, remittance basis etc' page(s) if, for all or part of the tax year in question, you were not resident in the UK. You may also need to fill it in if you were not domiciled in the UK and claiming the remittance basis during that tax year, or if you are a dual resident in the UK and another country. |

If you’re a sole trader, limited company director or unincorporated landlord, you may be able to fill in your tax return and submit it to HMRC using FreeAgent.

FreeAgent currently supports the Main Return (SA100), Employment (SA102), Self-employment (SA103) and UK property (SA105) sections of the Self Assessment tax return. You can find more information for sole traders, limited company directors and unincorporated landlords about filling your Self Assessment tax return using FreeAgent in our Knowledge Base.

If you need to complete any additional supplementary pages then you won't be able to use FreeAgent to submit your Self Assessment tax return. Instead, you will need to either complete your tax return on HMRC’s website or download and fill in the Main Return and all relevant supplementary pages before posting them to HMRC.

Whichever method you’re using, this guide should help you understand which pages you need to fill in and what information you need to provide in each.

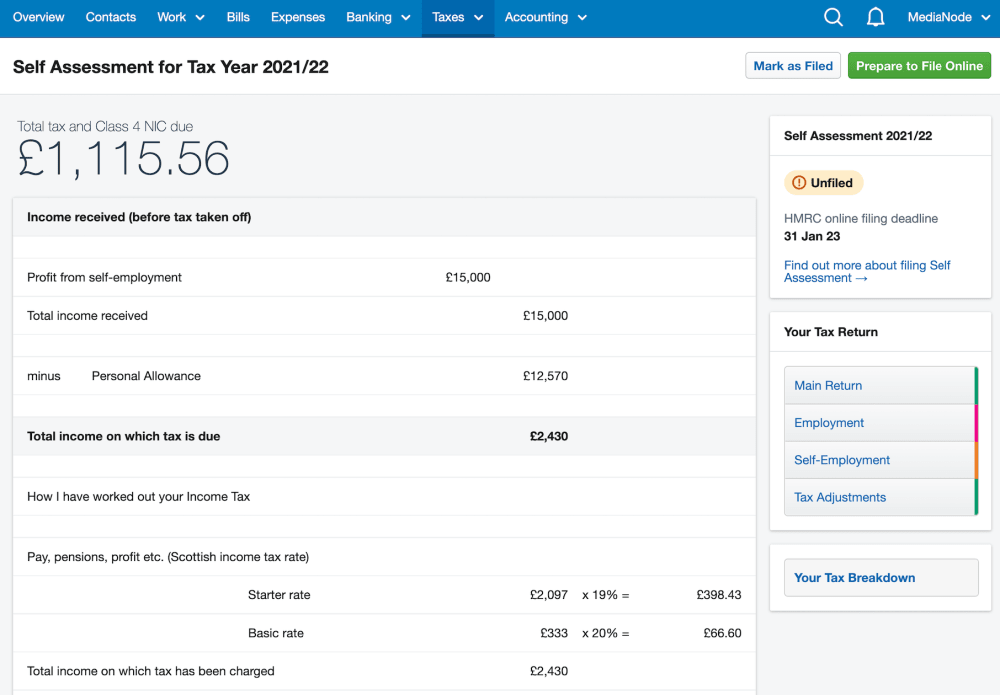

Completing the Main Return (SA100)

The SA100 is the main section of your Self Assessment tax return. To complete it, you’ll need to provide information including your income, pension contributions and any taxable state benefits you received (including the State Pension) during the tax year in question.

The SA100 section is split into the following sections:

- Starting your tax return

- What makes up your tax return

- Income

- Tax Reliefs

- Student Loan and Postgraduate Loan Repayments

- High Income Child Benefit Charge

- Marriage Allowance

- Finishing your tax return

We’ll cover each section in more detail below. HMRC also provides comprehensive notes on how to complete your SA100, which you can download from the SA100 page on HMRC’s website.

Section 1: Starting your tax return

This section lets HMRC know who you are. You’ll need to fill in your date of birth, name and address, contact telephone number and National Insurance number in the boxes provided.

Section 2: What makes up your tax return

You can use this section to let HMRC know which supplementary pages you intend to complete as part of your tax return. You may sometimes need to complete the same supplementary page more than once (for example, if you had two jobs during the tax year you’d have to fill out two Employment supplementary pages: one for each employment).

You can find more information about each of these pages in the ‘Completing any supplementary pages’ section below.

Section 3: Income

The information you provide in the ‘Income’ section of the SA100 lets HMRC know about the following types of income you received during the tax year in question.

Interest and dividends from UK banks and building societies

If you received any income in the form of interest from banks and building societies during the tax year in question, you should tell HMRC about it in this section. You should also include information about any dividend payments you received or were due to receive.

This information can usually be found on statements from your bank or building society and on dividend vouchers.

Pensions, annuities and state benefits

If you received income from a pension or received certain taxable state benefits during the tax year in question, you should tell HMRC about it in this section.

You will be asked for information about:

- your entitlement to the State Pension

- any lump sums you received from deferred State Pension payments

- any income you received from any other pensions and retirement annuities

- any tax you paid on income from other pensions and retirement annuities

You can usually find information about other pensions on a P60, or on an end-of-year certificate or other document issued by your pension provider.

You will also be asked for information about any taxable benefits you received during the tax year, including:

- Incapacity Benefit or contribution-based Employment and Support Allowance

- Jobseeker’s Allowance

- the total of any other taxable state benefits

If you received any taxable state benefits, the Department for Work and Pensions should issue you with a P60 or other similar form, which will contain the information you’ll need in order to complete this section.

Other UK income not included on supplementary pages

This section is for any taxable income that isn’t covered in the sections above or on any supplementary pages you complete. You should also enter any allowable expenses that relate to this income and any Income Tax that you’ve already paid on it.

There are boxes on the page for:

- the pre-tax total of this income

- your allowable expenses

- the amount of tax you’ve already paid on this income

- any benefits from pre-owned assets

This section covers a broad range of income, so the financial information you’ll need in order to complete it may vary. Be sure to refer to HMRC’s notes if you’re in any doubt about what you should or shouldn’t be including, or ask an accountant.

Section 4: Tax reliefs

This section of the SA100 covers tax relief for payments to pension schemes and charities, and for Blind Person’s Allowance.

Paying into registered pension schemes

This section is for payments you made to registered pension schemes during the tax year.

You should include payments to registered UK pension schemes and payments to overseas pension schemes in the boxes provided.

You are not usually required to include any contributions from an employer or payments you made to a pension scheme through your employer, as these are deducted from your pay before tax.

Your pension provider should provide you with a summary of your payments, either annually or on request.

Charitable giving

This section is for telling HMRC about any tax relief you claimed on contributions you made to charities during the tax year in question.

You should include both the total value of all the Gift Aid payments you made and the value of the ‘one-off’ Gift Aid payments you made in the boxes provided. You should not include any payments that you made under Payroll Giving.

You should also add any shares, securities or land that you donated to charity, as well as any donations you made to overseas charities, on which you wish to claim tax relief.

Blind Person’s Allowance

This section is for telling HMRC whether you claimed the Blind Person’s Allowance during the tax year. You should mark the appropriate box if you claimed this allowance. You can also enter details of the local authority with which you are registered as blind.

If your spouse or civil partner has claimed Blind Person’s Allowance but does not have enough taxable income to use it all and you want to claim the surplus, you can mark the relevant boxes.

Section 5: Student Loan and Postgraduate Loan repayments

This section lets you tell HMRC about any student loans you’re currently repaying and how much you repaid during the tax year.

If you received a letter from the Student Loans Company notifying you that repayment of an Income Contingent Loan began before the end of the tax year in question, you should mark the relevant box.

If you’re employed, you should add the total amount of Student Loan and/or Postgraduate Loan repayments that were deducted from your salary during the tax year in the appropriate boxes. You can find this information on your P60 or on individual payslips.

Section 6: High Income Child Benefit charge

You will usually only need to fill in this section if, during the tax year, you or your partner received Child Benefit and your individual income was over £50,000.

If this applies to you, fill in the total amount of Child Benefit that you or your partner received during the tax year and the number of children for whom you received Child Benefit. You can use the Child Benefit calculator on the HMRC website to calculate the total amount of Child Benefit you received.

Section 7: Marriage Allowance

You will only need to complete this section if one of the following scenarios applied to you during the tax year in question:

- Your income was less than the Personal Allowance and you wish to transfer some of your Personal Allowance to your spouse or civil partner, or

- You were a basic-rate taxpayer, and your spouse or civil partner received income that was less than the Personal Allowance, and they wish to transfer some of their Personal Allowance to you.

To do this, you’ll need to enter the relevant details into the appropriate boxes on the section.

Section 8: Finishing your tax return

The final section of the SA100 section lets HMRC know if you’ve had any tax ‘set off’ or refunded for the tax year in question.

If you haven’t paid enough tax during the tax year but don’t want HMRC to collect the tax owed by adjusting your tax code for the following year, you can indicate this by checking a box in this section. You can only do this if you owe less than £3,000 and are filing your tax return before 30th December.

You can also use this section to provide bank details if you’ve paid too much tax and are claiming a repayment. Be sure to ask your accountant if you’re in any doubt about which boxes you need to fill in.

Finally, if you have a tax advisor or accountant, this section allows you to provide HMRC with information about them.

Completing any required supplementary pages

Everyone who has to fill in a Self Assessment tax return has to complete an SA100 (the Main Return). Depending on your circumstances, you may also have to complete additional sections, which HMRC calls ‘supplementary pages’. HMRC provides helpsheets and notes on its website for each of these pages.

Supplementary pages currently supported in FreeAgent

FreeAgent currently supports the following supplementary pages. If you’re a sole trader or the director of a limited company, this means that if you need to complete either or both of these pages in addition to the Main Return and don’t need to complete any other supplementary pages, you can use FreeAgent to complete your Self Assessment tax return and submit it to HMRC.

Employment (SA102)

You may have to fill in the 'Employment' (SA102) section if you were an employee, director, office holder or agency worker during the tax year in question. HMRC requires you to complete a separate SA102 section for each employment, so if you had more than one job during the tax year, you will need to fill in multiple SA102 sections.

HMRC provides notes about the SA102 that may help you determine if you have to complete this section of the tax return. You can download these notes from the SA102 page on HMRC’s website.

Self-employment (SA103)

You may have to fill in the ‘Self-employment’ (SA103) section if you worked for yourself as a sole trader during the tax year in question. You may not need to do this if the income you received from self-employment was below £1,000.

HMRC provides notes about the SA103 that may help you determine if you have to complete this section. You can download these notes from the SA103 page on HMRC’s website.

UK property (SA105)

You may have to fill in the ‘UK property’ (SA105) section if you received income from UK property, including rent and other income from land you own or lease out. You may not need to do this if the income you received from property was below £1,000.

HMRC provides notes about the SA105 that may help you determine if you have to complete this section.

Other supplementary pages

The following supplementary pages are not currently supported in FreeAgent. This means that if you’re required to complete any of these pages in addition to the Main Return, unfortunately you cannot use FreeAgent to complete your Self Assessment tax return and submit it to HMRC.

Additional information (SA101)

You may need to fill in the ‘Additional information’ (SA101) section if you received less common kinds of income and tax reliefs during the tax year in question. These include:

- Married Couple’s Allowance (for couples where one partner was born before 6th April 1935)

- life insurance gains

- chargeable event gains

- Seafarer’s Earnings Deduction

- disclosed tax avoidance schemes

HMRC provides notes about the SA101 that may help you determine if you have to complete this section.

Partnership (SA104)

Each partner in a partnership must fill in the ‘Partnership’ (SA104) section of their Self Assessment tax return. In addition, one partner will have to complete a separate Partnership Tax Return (SA800) for the partnership.

HMRC provides notes about the SA104 that may help you determine if you have to complete this section.

Foreign (SA106)

You may have to fill in the ‘Foreign’ (SA106) section if, during the tax year in question, you:

- were entitled to foreign income. If this income is in respect of bank interests and/or dividends, you should record the amount in this section if it is £2,000 or more. If it is less than £2,000 you should record it on the Main Return page instead.

- received (or think you may have received) either income, a capital payment or a benefit from a person abroad as a result of any transfer of assets

You may also have to fill in this section if you want to claim relief for foreign tax paid during the tax year.

HMRC provides notes about the SA106 that may help you determine if you have to complete this section.

Trusts etc (SA107)

You may need to fill in the ‘Trusts etc’ (SA107) section if you received (or are treated as having received) income from a trust, settlement or the residue of a deceased person’s estate during the tax year.

This does not include cash lump sums or transfer of assets (otherwise known as capital distributions) that you received under a will.

HMRC provides notes about the SA107 that may help you determine if you have to complete this section.

Capital Gains summary (SA108)

You may need to fill in the ‘Capital Gains summary’ (SA108) section if you made any chargeable gains by selling certain assets during the tax year, including:

- stocks or shares

- land and property

- a business

HMRC provides notes about the SA108 that may help you determine if you have to complete this section.

Residence, remittance basis etc (SA109)

You may need to fill in the ‘Residence, remittance basis etc’ (SA109) section if, for all or part of the tax year in question, you were either:

- not resident in the UK

- not domiciled in the UK and claiming the remittance basis

- a dual resident in the UK and another country

HMRC provides notes about the SA109 that may help you determine if you have to complete this section.

Filing your Self Assessment with FreeAgent

If you’re a sole trader, limited company director or unincorporated landlord and you’re looking for a simple way to complete and file your Self Assessment tax return, our online accounting software might be the answer.

With support for the Main Return, the Employment page, the Self-employment page and the UK property page, FreeAgent takes the data you enter throughout the year to complete parts of your tax return automatically.

When it’s time to file your tax return, all that’s left for you to do is to check the information, add in the extra details and click the button to submit it directly to HMRC. Take a closer look at Self Assessment in FreeAgent and start your 30-day free trial today.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.