How to get a mortgage when you’re self-employed

Looking to get on the property ladder? You might be put off by the commonly held belief that getting a mortgage when you’re self-employed is almost impossible. Don’t believe a word of it!

The truth is that being self-employed does not make mortgage lenders any less likely to approve your application than if you were employed – you just have to be a little bit more organised in your approach to managing your finances.

This guide explains the steps you should take as a small business owner, freelancer or contractor to give yourself the best chance of having your mortgage application approved. It also highlights some common mistakes to avoid.

Jump to a section or read on to take it all in:

- There’s no such thing as a self-employed mortgage

- What were self-certification mortgages?

- Getting a mortgage: employed vs. self-employed

- Case study from a self-employed videographer

- How to keep your finances organised

- What documents do you need in order to prove your income for mortgage purposes?

- How many years of accounts do you need in order to get a mortgage?

- What type of business is it easiest to get a mortgage with?

- Other factors that will help you get the green light

- Remortgaging when you’re self-employed

- Self-employed mortgage pitfalls to look out for

First of all, let’s get something straight:

There’s no such thing as a self-employed mortgage!

Whether you’re employed or self-employed makes no difference to the range of mortgage products that you’re entitled to in the UK. Lenders just need to know about your ability to repay. Having a contracted salary from an employer is a great way to demonstrate this, but there are plenty of other ways to prove that you’re good for the money if you run your own business.

A lot of the confusion surrounding the concept of “self-employed mortgages” comes from the abolition of self-certification mortgages back in 2014.

What were self-certification mortgages?

Self-certification mortgages, or self-cert mortgages, enabled people to borrow money to buy a home without having to prove their income. Instead, applicants simply told the lender what they earned without the need for any proof to back it up. Can you guess what’s coming?

These types of mortgages were originally aimed at a minority of self-employed borrowers who found it difficult to prove their income, but they ended up being sold much more widely. Dishonest borrowers would exaggerate their income in order to secure a bigger mortgage with minimal checks and as a result, self-cert mortgages quickly earned the nickname “liar loans”.

Unsurprisingly, the Financial Conduct Authority (FCA) outlawed self-certification mortgages in 2014, making it more difficult - but certainly not impossible - for self-employed people to secure a mortgage.

Getting a mortgage: employed vs. self-employed

Mortgage lenders are required by law to be confident that anyone they approve for a mortgage has the ability to repay. It’s up to you, the borrower, to prove that you’re likely to be able to keep up with repayments and - for better or worse - this can be a little bit easier to do if you’re employed.

Employed borrowers

Employees generally have a contracted salary with their employer and, through PAYE, they can produce payslips and P60s to prove their income relatively easily. Lenders can use this evidence to confidently work out how much income the borrower will have to contribute towards their mortgage repayments.

From the employee’s perspective, the PAYE system is automated: at the end of the month, tax is deducted from their salary and the rest is individual profit. This is a very neat and tidy way for the mortgage lender to draw a conclusion about how much money the employee will be able to pay back.

Self-employed borrowers

If you’re self-employed, keeping your finances neat and tidy and working out profit accurately is a little more complicated. With various taxes, expenses, bills, invoices, dividends and much more on top of all that, it can be difficult to prove to a lender that the money you earn would be enough to cover mortgage repayments.

Organisation is key and if you’re considering buying a house in the near future it’s never too early to start looking for a better way of organising your accounts and pre-empting the questions that lenders might ask about your income.

Seeking advice on getting a mortgage

There are a number of mortgage lenders who offer products specifically designed for self-employed workers. Mainstream lenders also routinely lend to self-employed workers, so don’t be put off.

A mortgage broker might be able to guide you in the right direction by letting you know which lenders are good with self-employed borrowers, which lenders take retained profits into account, which lenders accept less than two years of accounts and where to get the best rate. Remember that using a broker may add to the cost of the mortgage application process.

How to keep your finances organised

As soon as you decide that you want to apply for a mortgage, you should start getting your accounts in order. There are a few tried and tested ways to do this:

Hire an accountant

Hiring an accountant is an obvious way to get your accounts in order. A few mortgage lenders might even require you to have a qualified accountant prepare your financial information, especially if your accounts are complicated. If you get your accounts prepared by an accountant, both you and the lender can be confident that the figures are accurate - but that’s not the end of it!

Understand your figures

Being overly reliant on an accountant can be dangerous. If you can’t demonstrate to the lender that you know what goes on with the money inside your own business then they’ll probably be reluctant to hand over any of their own money to you.

For example, if your cashflow has dipped at some point then the lender might ask you to explain why. Shrugging it off isn’t going to give them confidence that they can trust you with a loan, but if you can explain your business finances clearly, they’re likely to be more confident in you.

Use accounting software

Using FreeAgent’s accounting software is a great way to keep your finances organised and provide evidence to mortgage lenders of your business finances.

The dashboard overview brings together all your business’s incoming and outgoing money in one place, allowing you to keep track of your cashflow at any moment in time. You can also see at a glance if your invoices have been paid, are due or are overdue, so you can chase any late payers quickly and get your finances in a good place ahead of submitting your mortgage application.

FreeAgent’s unique tax timeline tells you when your next tax bill is due and how much you’ll have to pay, and your outgoing expenses and bills are also clearly visible, giving you a good opportunity to tighten the purse strings before the lender looks closely at your spending habits.

All this information, as well as the ability to print your most important financial reports, will not only keep you organised and give you great insight into how your business is performing but will be compelling evidence for mortgage lenders of your ability to repay.

What documents do you need in order to prove your income for mortgage purposes?

The method you’ll need to use to prove your income varies depending on your business structure and how long you’ve been self-employed. However, there are a few documents that are common to most mortgage applications:

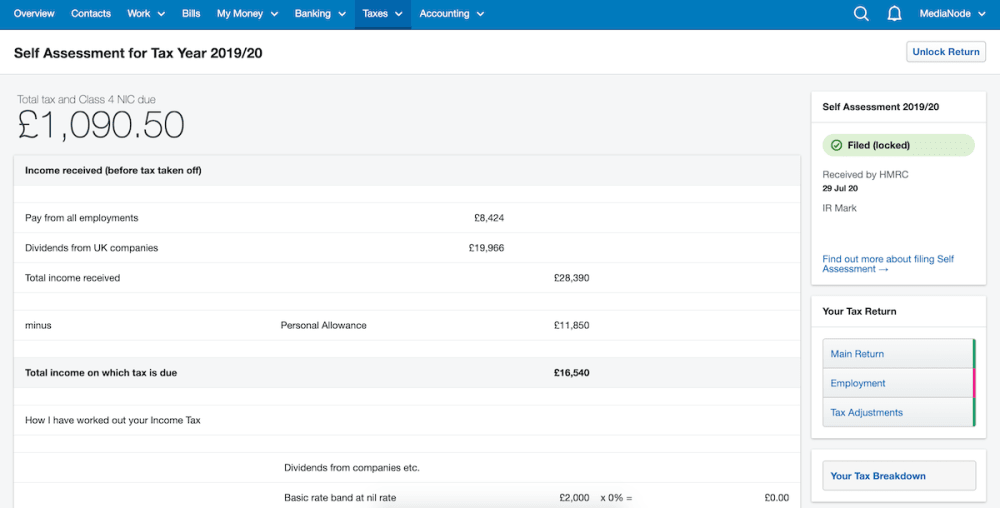

Your SA302 form

The SA302 - the form that shows your tax breakdown based on your latest Self Assessment submission - is the most commonly requested form when you apply for a mortgage as a self-employed business owner. Most lenders will ask for three years of SA302s for evidence of sustained income. It’s worth checking if the mortgage lender accepts documents that you’ve printed yourself or if they require a covering letter from an HMRC official. If the latter is the case, you should get in touch with HMRC directly.

Getting your tax breakdown in FreeAgent

The information displayed in the ‘Your Tax Breakdown’ page in the Self Assessment section of your FreeAgent account serves as the equivalent of the SA302 form. Most mortgage lenders will accept tax breakdown information from FreeAgent in place of the official SA302 form so if you use FreeAgent, you can print off the information directly from the software.

Take a closer look at Self Assessment in FreeAgent to find out more.

Getting your SA302 from HMRC

If your lender does require an SA302 from HMRC, here’s how to get it:

- Log in to your HMRC online account and go to “Self Assessment”

- Go to “More Self Assessment Details”

- Click on “Get your SA302 tax calculation”

- Click on the option to print the form

Note that you may not be able to print this form from your HMRC account if you’ve submitted your tax return directly to HMRC through software. In this case you’ll just have to print the equivalent form from the software and a tax year overview from your HMRC online account. If your mortgage provider will not accept this document printed from the software, you’ll need to request a paper copy of your SA302 from HMRC.

Proof of income

The documents required to prove your income will vary from lender to lender. Some might ask for certified accounts certificates signed by an accountant, whereas others might be satisfied with a combination of bank statements, profit and loss reports and balance sheets.

The key thing to do here is to get your accounts in order and make sure you can understand what they’re telling you. If you can’t make head nor tail of your own accounts you can’t expect the lender to!

Bank statements

Bank statements can be used as proof of income but they can also be used for other purposes, such as determining your expenditure. If you’re getting a mortgage with a bank that you have a current or business account with, they may have access to this information already. They might not ask you to provide any statements, but be aware that they will be looking at your account.

Proof of deposit

Understandably, the lender will want to see proof that you have the deposit that you say that you have. It’s likely that they’ll ask for evidence such as a recent bank statement.

Outgoings

Most mortgage applicants have to complete some kind of expenditure form that includes details of any regular outgoings. Items such as debt repayments, childcare costs, pension contributions and subscriptions will all be used by the lender for their calculation.

How many years of accounts do you need in order to get a mortgage?

If you’ve been self-employed for more than three years, you shouldn’t find too much extra resistance from an average lender simply because you’re self-employed, as long as you’ve kept your accounts up to date and you have proof that you’ve maintained a healthy cashflow. However, any less than three years of accounts and you might find it a bit trickier.

If you’re self-employed with two years of accounts

Some lenders will be more willing than others to look at evidence of income from two years’ worth of accounts. If you’re in this position, you should aim to get as much of the proof that you need in place in order to prove that you can meet repayments. A bigger deposit and a track record of steady work should also help your application.

If you’re self-employed with one year of accounts

With one year of accounts, it can be difficult for the lender to confidently determine that you’ll be able to maintain your income. If you have contracts in place for future work or evidence of a steady stream of work from reliable clients, then this might help your application.

Be prepared to shop around for a lender and don’t get too disheartened if you have an application rejected. At least you’ve gone to the effort of getting your accounts in order ready for the next time!

Self-employed with no accounts

If you’ve been trading for less than a year and have yet to submit your first tax return, then unfortunately it will be difficult to provide the evidence needed to prove that you’ll be able to keep up mortgage repayments. Remember that the mortgage lender is required by the FCA to prove that they’ve lent money responsibly, and without any evidence of a self-employed person’s accounts this will be difficult.

If you are near to the end of your first trading year and have had a fruitful few months, you could consider making an initial application and getting the mortgage approved in principle based on what you think your income will be. This will save a bit of time when you eventually do file your first year of accounts with HMRC, as an agreement in principle usually lasts for a few months.

What type of business is it easiest to get a mortgage with?

Sole trader

Income for sole traders is pretty straightforward. If you’re a sole trader, you and your business are legally the same entity and all profits belong to you. It’s these profits that a mortgage lender will assess. Your SA302 will show your total income received and total tax due and your lender will be likely to look at this information alongside your business accounts.

Lenders will be looking to see if your income has increased or decreased in recent years. If it has increased, they may take the average income for the past two or three years into account. However, if it has decreased, lenders might look at the latest and lowest figures instead.

FreeAgent’s cashflow chart is a great way to illustrate increasing income from all your business bank accounts. Bank feeds are available for most banks so your transactions are automatically pulled into your account and reflected in your cashflow. The lender will also be able to see any overdue invoices to determine if there’s likely to be money coming in in the near future.

Limited company

For limited companies, the business is a separate legal entity from the individual so the business’s profits and the individual’s profits are considered separately.

It’s the individual’s income from a basic salary and dividend payments that most lenders will focus on, so make sure you have a clear record of both of these for the last few years. Your business accounts are also likely to be looked at as an indication of your reliability, so make sure they’re up to date.

Some lenders might also take retained profit (the profit you keep in the business rather than paying out as salary or dividends) into account, so you might want to check this with the lender before you apply.

Partnership or Limited Liability Partnership (LLP)

For partnerships, lenders will take into account each partner’s share of the profit - so make sure your accounts clearly reflect this.

Other factors that will help you get the green light

A track record of regular work

If you have good relationships with a range of clients and can prove that you have had repeat business with them, this should work in your favour.

Proof of steady work in the future

If you have future work planned in, this should be a great boost to your chances of convincing the lender that you’re a safe pair of hands. You might even be asked, particularly if you are a contractor, to show work you have lined up for the future in order to prove that you can maintain or improve on the income from previous years.

Healthy deposit

When you first start thinking about getting a mortgage, use a mortgage calculator to work out the deposit you’ll need - then get saving! The bigger your deposit, the better your chances of securing the mortgage you want.

Good credit history

Lenders won’t just run a credit check on you, they’ll also run a credit check on your business. Sort out any unpaid debts ahead of applying and consider running a credit check from a trusted service on yourself to see what might be in store. It might be a good idea to pay off any outstanding bills before doing this.

Remortgaging when you’re self-employed

Once you’ve secured your mortgage, the process isn’t over for good. It’s inevitable that you’ll be looking to remortgage at some point down the line in order to move home or to get a better deal. Be aware that you’ll probably have to jump through all the hoops you faced the first time round to prove your ability to continue keeping up with your repayments - so make sure you keep your accounts up to date!

Self-employed mortgage pitfalls to look out for

There are a few things that you might be doing in the day-to-day running of your business that could come back to bite you when you start applying for a mortgage.

Beware of reducing your taxable income

If your accountant uses legitimate methods to reduce your taxable income, it might work against you in the mortgage application process. Lenders will be using this figure to calculate how much they can lend you: the higher your taxable income, the more you should be able to borrow. In the run-up to applying, you might want to ask your accountant to hold off on reductions in order to maximise your income.

Make sure the lender takes into account all of your income

If you’re self-employed and also earn money through the PAYE system, ask the lender in advance how they would view your income. You want to be sure that they take into account all of your income, not just your income from self-employment.

Get on the electoral register

If you’re not registered to vote you could run into trouble as some lenders include this in their background checks. You can find out more about getting on the electoral register here.

Shop around

Don’t jump at the first mortgage deal because you’ve been approved! Shop around for the best rate. Remember that applications can be time-consuming - and sometimes costly - so do your research early on to narrow down your choice and reduce the time you spend on applying.

Limit your outgoings

Extravagant expenses might work against you when the lender goes through your outgoings with a magnifying glass, so cut back on things that might be deemed luxuries in the months running up to applying for a mortgage – that new laptop might have to wait!

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.

12th July 2023