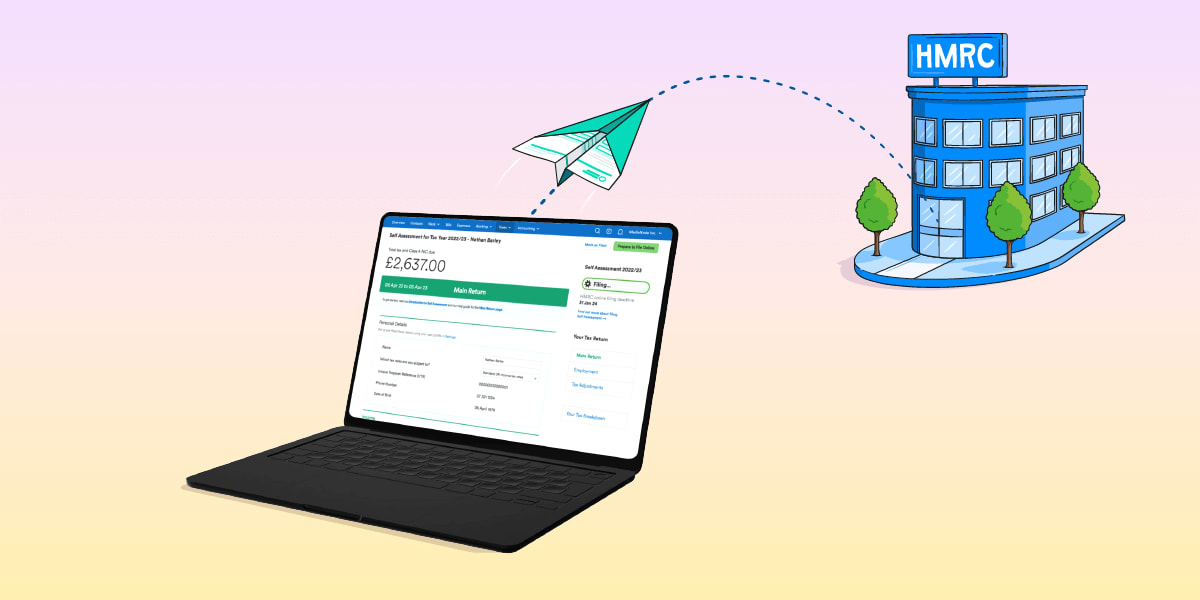

File Self Assessment with confidence

Find out everything you need to know to feel confident about Self Assessment, including key deadlines, who needs to file and how to complete your tax return.

Lacking cashflow confidence? No idea what Making Tax Digital means for you? Don't worry, we've got you covered with handy guides to help you manage your business better.

Find out everything you need to know about Making Tax Digital, including whether the legislation applies to you, key deadlines and what you need to do to comply.

Find out everything you need to know to feel confident about Self Assessment, including key deadlines, who needs to file and how to complete your tax return.

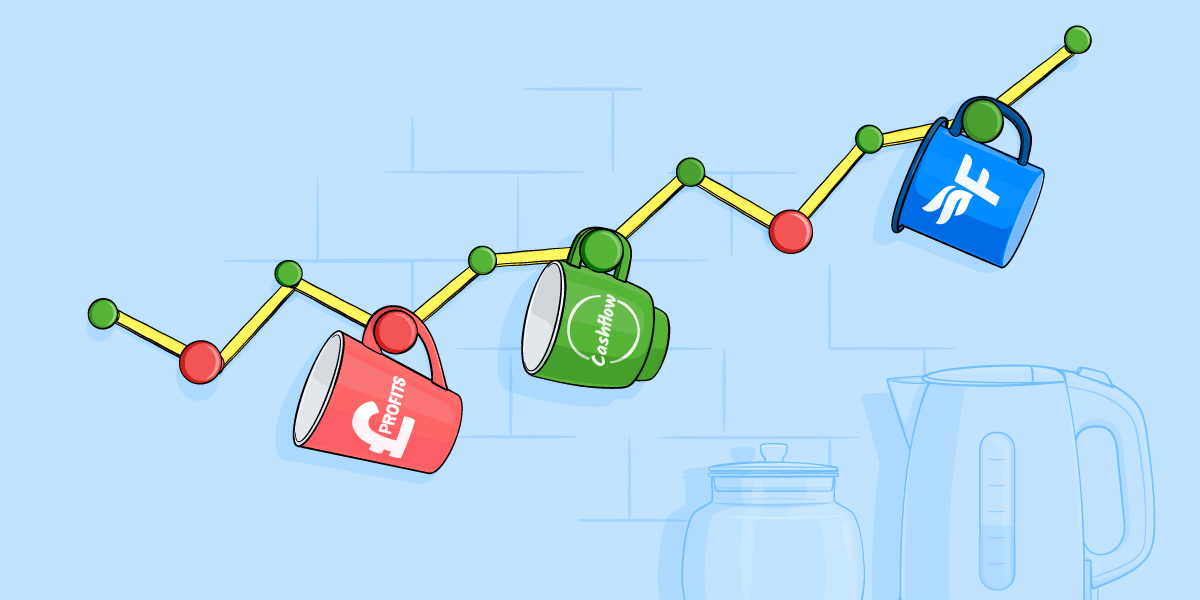

In this series of guides, we'll explain everything you need to know about cashflow, including what it is, why it's important to your business and how to calculate it.

Whether you’re a startup or an established company looking to expand, understanding the responsibilities and best practices of being an employer is crucial.

Are you a landlord? Whether you're looking to let your first property or are an established landlord, we've got lots of useful information about managing your property finances.

Set out on your own startup adventure with our handy guides to help you find the way.

If cashflow's feeling tight, try taking a look through our helpful content for some ideas, advice and guidance on how your business can not just survive but thrive in lean times.

Expert tips to help you manage and grow your small business like a boss.

Take control of your finances with our bookkeeping tips for small businesses and freelancers.

Find out more about which small business expenses are allowable for tax relief from HMRC.

Discover what you should include on your invoices, how to chase late payments and ways to get paid faster.

Find out all about VAT registration, the VAT Flat Rate Scheme, and filing your VAT return.