Guide

Do you have to file a Self Assessment tax return? Find out if HMRC is expecting a tax return from you this year.

Find out everything you need to know to feel confident about Self Assessment, including key deadlines, who needs to file and how to complete your tax return. Learn more about how FreeAgent can help.

Not sure where to start with your tax return? Browse through our topics and guides below to find the information you’re looking for.

Find out if HMRC is expecting a tax return from you this year.

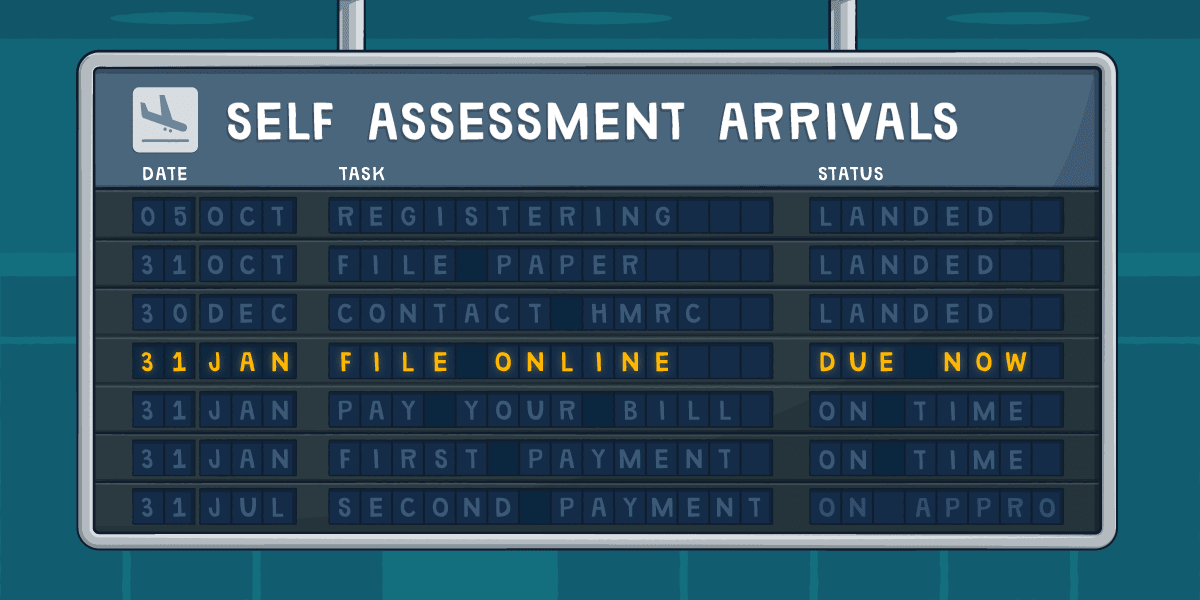

Our guide to the key Self Assessment dates throughout the year should help you avoid any nasty surprises.

Find out how and when to register for Self Assessment, and how the registration process might vary depending on your circumstances.

Payments on account often catch business owners out. Here’s everything you need to know.

A list of all the things that you’ll need to have to hand in order to complete your tax return.

Follow these useful tips to avoid the most common mistakes that people make in the rush to file before the deadline.

Find out which sections of the tax return you’ll need to complete and what information you’ll need to provide.

Find out what income you need to pay tax on - as well as the income you don’t!

Learn more about the different ways you can pay your tax bill and how long it will take for your payment to reach HMRC.

Here’s how you can foster a winning relationship with your accountant during Self Assessment season.

It’s going to be OK! If 31st January has been and gone, follow the tips in this guide to help minimise the impact of missing the deadline.

Made a mistake on your tax return? Here’s how to fix it.

Read more about Self Assessment on our blog.

Calling all keen beans: get ahead of the game and file your tax return early.

This is what Making Tax Digital will actually look like for sole traders and landlords.

In the meantime, feel free to browse for more handy content and useful ideas.

Download your all-in-one guide to completing each step of your Self Assessment tax return.

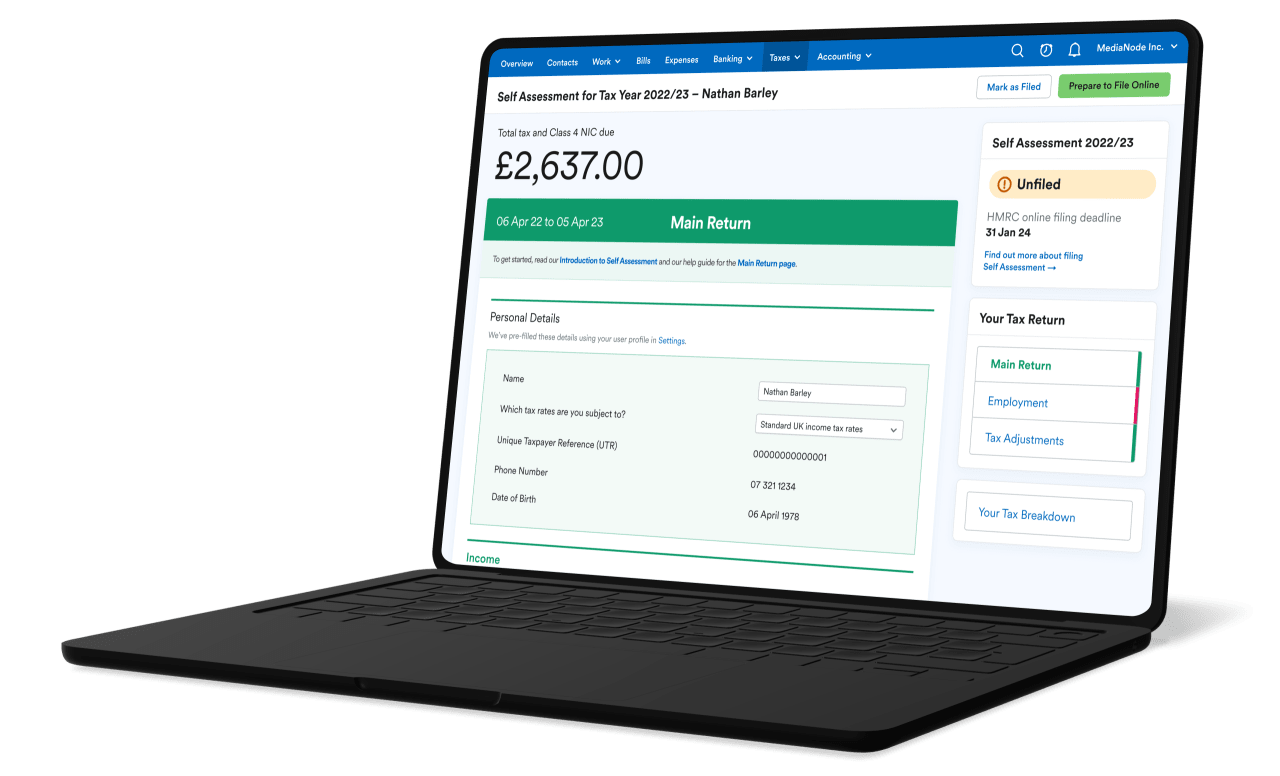

If you're a sole trader, limited company director or unincorporated landlord, FreeAgent works away in the background to calculate your Self Assessment liability and prepare your tax return.

Get Self Assessment tax-confident Already a FreeAgent customer?

Our Knowledge Base has lots of helpful information about filing your Self Assessment tax return using FreeAgent.