GPSR: get to grips with the EU’s new safety regulations for retailers

The EU’s General Product Safety Regulation has hit small businesses hard. Here’s how you can keep sel...

The EU’s General Product Safety Regulation has hit small businesses hard. Here’s how you can keep sel...

Landlords - did you know you can claim a tax deduction when replacing certain household items? Here’s...

Business owners reveal their top tips and tricks for saving time and smashing their goals.

Continuing Professional Development (CPD) is important for your accounting or bookkeeping career. Her...

Accountants and their landlord clients can now record different ownership splits across multiple prop...

HMRC is waiving late payment penalties for some business owners - find out if you’re affected.

A quick reminder of the rules for keeping records of your business expenses.

These are the steps you can take if you disagree with a Self Assessment penalty.

Attracting and retaining talent in the accounting industry has never been more challenging. Here are ...

Your guide to the new basis period rules... and whether you need to do anything.

Even the most organised business owners can occasionally find themselves struggling to pay their Self...

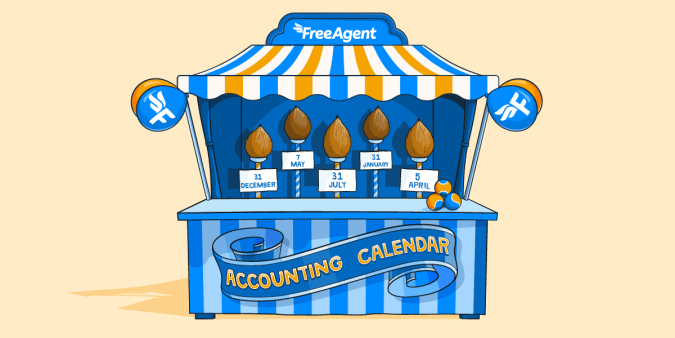

Roll up, roll up! It’s time to get this year’s important tax deadlines in the diary.

Find out the types of tax relief you might be able to claim for and how to claim this to reduce your ...

How should you record key incomings and outgoings on your Self Assessment tax return?

We’re here to guide you through all the basics, while our Chief Accountant answers your FAQs.

FreeAgent brings you a soothing 60-minute video soundtrack, to boost your focus as you prepare to file.

We recap the announced changes to employment rights including unfair dismissal, flexible working requ...

You asked? We delivered! This year, thanks to your suggestions to make FreeAgent work harder for you ...

From office parties to festive gifts, here are the expenses your business could be claiming tax relie...

Frequently asked questions from sole traders and limited company directors.

Time for your business to shine on social.

We explain what information HMRC needs to calculate your tax bill, when you can see how much you owe ...

We’ve put together some useful tips that should help you stay cool as a cucumber all the way to 31st ...

FreeAgent has been named Friendliest Software of the Year at the ICB LUCA Awards 2024 - for the fifth...

We spoke to Brad, George, Sandra and Tobias to find out what brought them back.

Record your outgoings at warp speed with Smart Capture for bills.

Government confirms MTD for Income Tax will start rolling out in just 18 months. Find out what prepar...

Changes to National Insurance and Business Rates, a new Corporate Tax roadmap, and more.

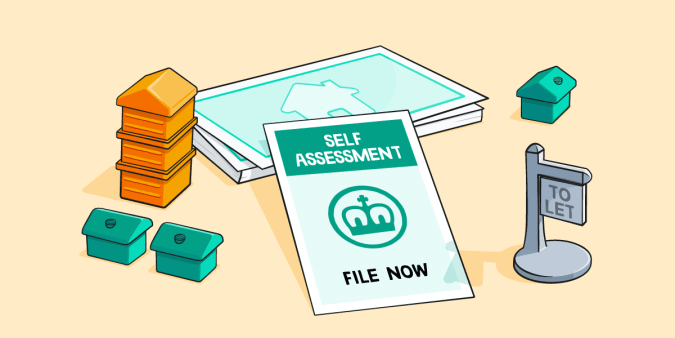

A tour of the current rules for furnished holiday lets and the changes coming in 2025.

An end to Section 21 evictions, a crackdown on bidding wars, a new ombudsman: how can you prepare?