Making Tax Digital: what you need to know to get it done

Doing starts with knowing. Here you’ll find clear answers on who’s affected by the legislation, when the key deadlines are and what to do next.

Accountant or bookkeeper? Visit our MTD information hub for a range of resources.

What is it and when is it happening?

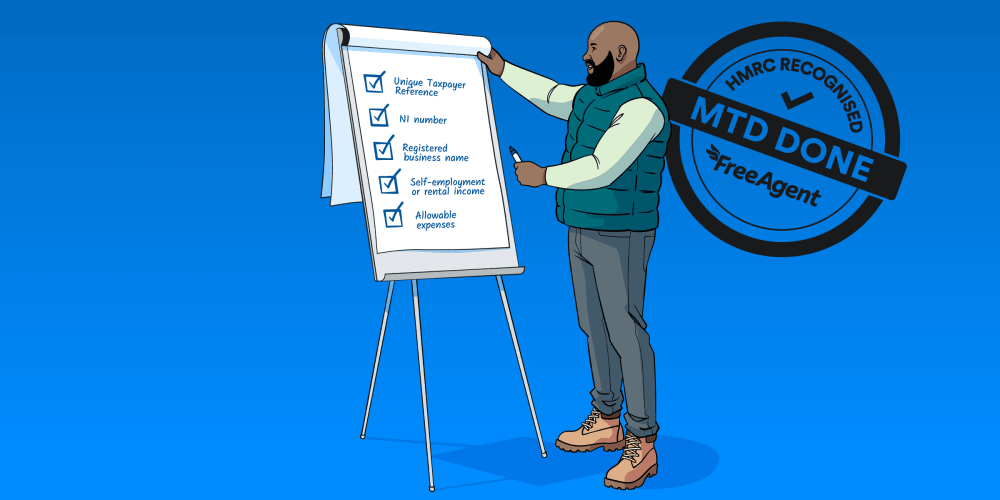

Making Tax Digital (MTD) is the government’s initiative to implement a fully digital tax system in the UK for Income Tax and for VAT (MTD for VAT arrived in 2022). Taxpayers will need to keep digital records and use MTD-compatible software to make their tax submissions electronically.

April 2022

MTD for VAT applies to all VAT-registered businesses

April 2026

MTD for Income Tax applies to most self-employed individuals and landlords with qualifying income over £50,000

April 2027

MTD for Income Tax will apply to most self-employed individuals and landlords with qualifying income over £30,000

April 2028

MTD for Income Tax will apply to most self-employed individuals and landlords with qualifying income over £20,000

Helpful guides to Making Tax Digital

Get on top of Making Tax Digital for Income Tax with our library of guides.

Year one of MTD for Income Tax: a step by step guide

Blog

Here’s what MTD for Income Tax will actually look like for sole traders and landlords.

How do I sign up for MTD for Income Tax?

Guide

Signing up is a manual process - HMRC will not do it for you. But don’t worry, this guide is here to help.

14 MTD for Income Tax terms you need to know

Guide

Qualifying income, quarterly updates, penalty points: master the jargon with our simple MTD glossary.

MTD for Income Tax: qualifying income explained

Guide

Learn what counts as qualifying income and how HMRC uses it to decide whether you need to follow the new rules.

How to efficiently manage multiple income streams

Guide

Are you a sole trader and a landlord? Got more than one small business? This guide’s for you.

MTD for Income Tax: what landlords need to know

Guide

Find out everything landlords need to know about Making Tax Digital (MTD) for Income Tax.

Making Tax Digital for Income Tax: 12 common myths busted

Blog

Urban legends aren’t going to help you prepare for Making Tax Digital for Income Tax, but we can.

Everything you need to submit your quarterly updates and final declaration

Guide

Mistakes to avoid when filing your MTD quarterly updates and final declaration

Guide

Here’s how you can dodge some common Making Tax Digital filing errors.

MTD for Income Tax: penalties and how to avoid them

Guide

We explain the new rules around fines - so you don’t get caught out.

MTD for Income Tax: what does it mean for you?

Guide

Qualifying income, quarterly updates, penalty points: master the jargon with our simple MTD dictionary.

Events and webinars

MTD quarterly updates cracked: how to file in FreeAgent

Live webinar

In this short webinar, we’ll take you through the simple steps you need to follow to file quarterly updates to HMRC.

MTD for Income Tax: your step-by-step guide to getting started

On-demand webinar

This simple webinar will help you register for Making Tax Digital for Income Tax and connect your software to HMRC. [15 mins]

Landlords: get MTD done with FreeAgent

Webinar recording

In this webinar for landlords, we de-mystify how you’ll have to submit your information to HMRC and show what MTD for Income Tax will look like in FreeAgent. [30 mins]

MTD for Income Tax news

6 April 2026

MTD lessons from people who’ve already filedTips from people like you about how to manage MTD for Income Tax.

Tips, news and inspiration for every small business

Thank you for signing up, we'll be in touch soon.

In the meantime, feel free to browse for more handy content and useful ideas.

Getting MTD done with Dom

‘There’s no trick to your taxes’

The magician

Chris Wall feels confident he’s ready for MTD, thanks to FreeAgent.

‘I know very little about MTD’

The gardener

Emma Cooper is just starting to dig into what the new tax rules will mean for her.

‘MTD is coming, so get prepared’

The accountant

Bright Ideas Accountancy is working hard to get clients ready - and bust MTD myths.

‘Some are frightened - but I’m ready’

The producer

At the studio where ‘Blue Monday’ was conceived, Dean Glover isn’t feeling down about MTD.

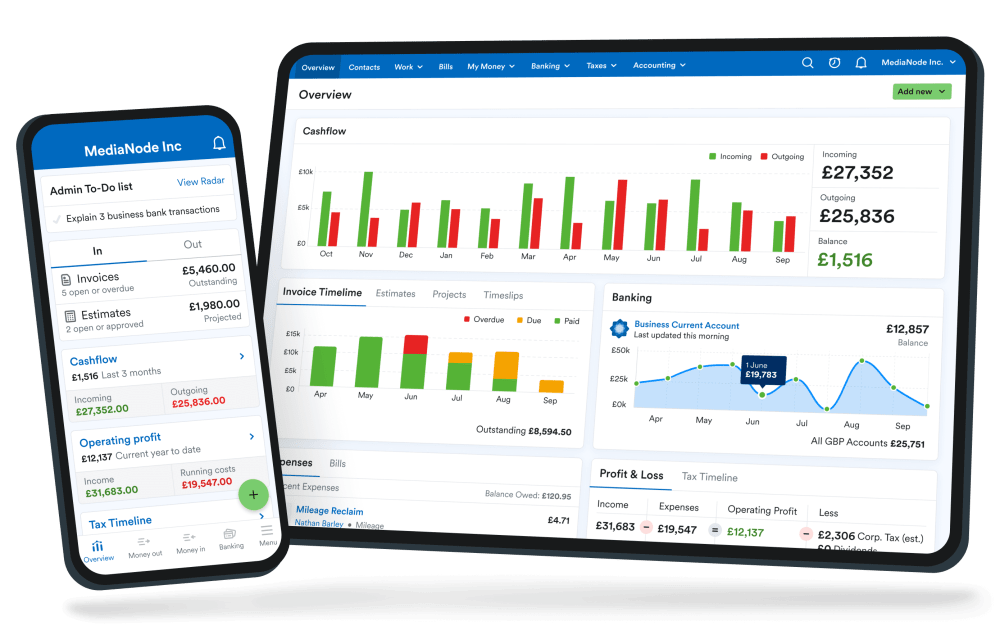

FreeAgent can help you prepare for Making Tax Digital

FreeAgent’s powerful automation features can help get your accounts in order for digital filing with minimal hassle. Check out all the other ways FreeAgent can help you stay on top of your business finances.

Accountants and bookkeepers, join our free Partner Programme and access exclusive discounts for your clients.