How to write great invoices

Find out what you should include in your invoices, how to chase unpaid invoices and how to get paid faster.

Invoicing basics: what to include in your invoice template

Are you including all of the things HMRC requires on your invoice template? FreeAgent's Chief Accountant Emily Coltman outlines HMRC's criteria in this handy guide.

Invoicing guides

Late payment excuses and how to defeat them

Some clients will try these classic excuses to get away with paying you late. Here's how to come back at them to increase your chances of getting paid on time.

Getting the VAT details right on your invoices

Are you including the required VAT details on your invoice? This guide helps you double-check.

Making it easy for your customers to pay

If you don’t invoice your customers, they can’t pay you! Here are some tips on how to make it simple for your customers to pay you.

Dealing with late payment of invoices: how to get over the awkwardness

Dreading that phone call to a late-paying client? Here’s how to make the conversation feel less awkward.

Five types of late-paying clients (and how to deal with them)

Here are five common examples of late-paying clients and how to work with them when it comes to getting your outstanding invoices paid.

Streamline getting paid

Give your customers more ways to pay with Tyl by NatWest, Stripe, GoCardless and PayPal

Take the turbulence out of the payment process for you and your customers.

Other Topics

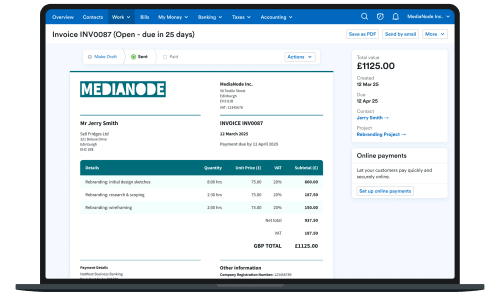

Simple invoice software that helps get you paid faster

Get paid online by credit/debit card, Direct Debit or PayPal.

Take a tour of invoicing in FreeAgent