What rate of VAT should you charge?

VAT is a tax on sales, but not all sales are subject to VAT - and not all those that are have the same rate of VAT!

Sales being “subject to VAT” just means that if the business making those sales is VAT-registered then they will charge output VAT at the appropriate rate to their customers on those sales. Businesses that aren’t registered for VAT don’t charge output VAT to their customers on any of their sales.

What are the different rates of VAT?

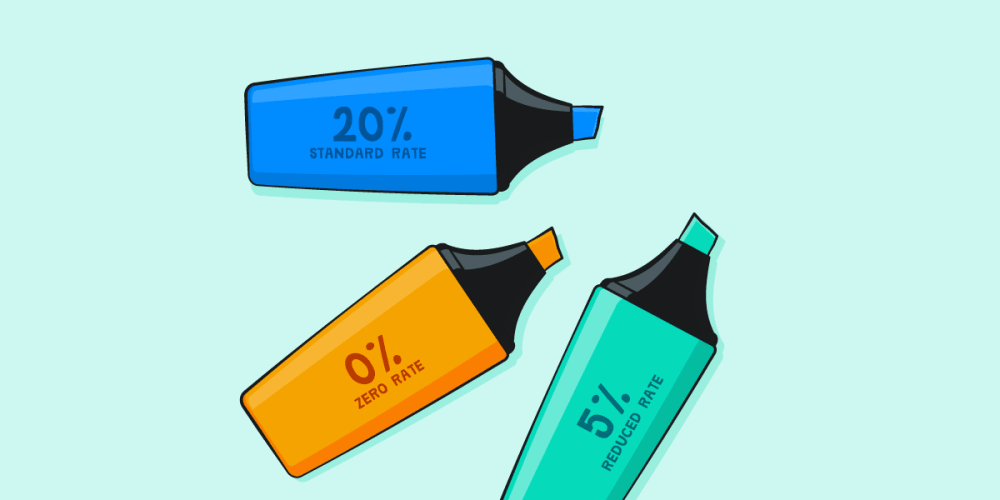

Standard rate

Most sales of goods and services in the UK are subject to VAT at the standard rate of 20%. You can keep up to date by checking the current standard VAT rate, along with the other rates, on our UK tax rate tracker. If you’re catching up with your bookkeeping in FreeAgent, historic rates are also available through FreeAgent’s digital VAT software.

One common source of confusion when it comes to the standard rate of VAT is food and drink. Although food and drink is often zero-rated for VAT, there are many exceptions where the standard rate applies instead. These include:

- catering and hot food (including hot takeaways)

- snacks such as crisps, confectionery and ice cream

- alcoholic drinks

- soft drinks

- sports drinks

Reduced rate

Some goods and services are subject to VAT at the reduced rate of 5%. These include a range of items like domestic gas and electricity, children’s car safety seats and products to help people stop smoking, such as nicotine patches.

Zero-rated

There are also some goods and services that are zero-rated for VAT, which means that no VAT is paid or can be reclaimed on them. Although the rate of VAT is 0%, it’s important to be aware that these goods and services are still considered to be subject to VAT.

Zero-rated goods and services include:

- baby and children’s clothes

- printed materials, such as books, magazines and newspapers

- travel fares, such as flights and train tickets

While this list seems fairly straightforward, there are some anomalies to be aware of. As printed material is zero-rated, for example, you may be tempted to assume that the printing of letterheads and posters is also zero-rated. However, it’s actually standard-rated. Another common example is car parking tickets. Even though most travel is zero-rated for VAT, car parking tickets are standard-rated.

If you’re unsure about the rate of VAT applied to certain goods or services, check HMRC’s website or ask your accountant.

Once you know the rate of VAT you need to charge for goods or services you can check the amount using our VAT calculator.

What are VATable sales?

Sales of standard-rated, reduced-rated and zero-rated goods and services all count as VATable sales. When you’re checking your annual sales to see if they exceed the VAT limit (£90,000 from 1st April 2024), you need to add up your standard-rated, reduced-rated and zero-rated sales.

Don’t be tempted to leave out zero-rated sales thinking they’re not subject to VAT. Remember that zero-rated sales are still subject to VAT - just at a rate of 0%! The sales that you can leave out are referred to as VAT-exempt.

If your VATable sales exceed the VAT limit - or are close to doing so - you will need to register your business for VAT.

What are VAT-exempt sales?

A sale being exempt from VAT is not the same as it being zero-rated.

While no VAT is charged at all on VAT-exempt sales, VAT is charged at 0% on zero-rated sales.

When you add up your VATable sales to see if they’re close to exceeding the VAT limit, you should include zero-rated sales and exclude exempt sales.

If your business only ever makes exempt sales, you’ll never be able to register for VAT, because you won’t make any VATable sales.

Items that are exempt from VAT include:

- education and vocational training

- medical care provided by a hospital, hospice or nursing home, as well as health services provided by doctors, dentists, opticians, pharmacists etc.

- postage stamps

- insurance

- TV licenses

- gambling costs

- financial services, such as loans, deposits and shares

But guess what? There are anomalies here as well! The services provided by pharmacists, for example, are VAT-exempt but the dispensing of prescriptions by pharmacists is zero-rated. Always check with HMRC or with your accountant if you’re not sure.

What’s outside the scope of UK VAT?

There’s another category to add to the list: sales that are outside the scope of the UK VAT system altogether.

As you might expect, this category includes some sales to customers abroad, but it also includes some UK services. Sales of vehicle MOTs are outside the scope of UK VAT, for example.

As with VAT-exempt sales, you shouldn’t include sales that are outside the scope of UK VAT when you add up your VATable sales to see if you need to register for VAT.

As you’ve probably noticed, there are many anomalies when it comes to VAT and this makes it a complicated area! When it comes to VAT rates, it pays to be very careful and to always take professional advice!

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.

29th March 2024