Everything you need to know about registering for VAT

VAT can be intimidating for anyone who runs their own small business, especially those who are already struggling with paperwork and are unsure of HMRC’s rules. Our guide explains what VAT is, how it affects your business and when you need to register.

A quick introduction to VAT

VAT is short for ‘Value Added Tax’, and is charged on most sales of goods and services in the UK.

When your business makes sales, you don’t charge VAT to your customers unless you’re registered with HMRC to do so. Sales on which VAT would normally be charged are called “taxable sales” or “VATable sales”. Sales that are exempt from VAT, or outside the scope of UK VAT, are not taxable sales.

You only have to register your business if its annual taxable sales are over the limit set by HMRC which is £90,000 from 1st April 2024.

When do you need to register for VAT?

If your annual taxable sales are above £90,000 per year - or they are set to pass that limit in the next 30 days - then you must register for VAT. This is called compulsory registration.

In some cases you may wish to register before you reach the threshold. This is called voluntary registration and it can help your cashflow, because being registered for VAT allows your business to claim back input VAT on its costs. However, if your customers are members of the general public or small businesses that aren’t registered for VAT, it may not be a good idea to register voluntarily, as you would have to charge your customers VAT which they wouldn’t be able to claim back. This could result in many of your customers paying more for the same goods or services.

HMRC has released a tool to help you estimate what registering for VAT might mean for your business. If you are required to register for VAT, this can help you plan ahead. If you are thinking of voluntary registration, it can help you make your decision. Before you use the tool, you’ll need some information on your sales and costs figures for goods and services sold in the UK. If you have a FreeAgent account, this information will be available in your Profit and Loss report.

How to register for VAT in the UK

Most people register for VAT online. If HMRC accepts your application for registration, they will send you a certificate which will also show your business’s unique VAT reference number.

What happens after you register?

Once your business is registered for VAT, then it has to charge VAT on all the taxable sales it makes to its customers. The VAT you charge to your customers is called ‘output VAT’. You can use our VAT calculator to work out how much output VAT you should charge.

Your business will also be able to reclaim some of the VAT that its suppliers charge. Bear in mind that there are some supplies on which you won’t be able to reclaim VAT, such as entertaining anyone other than staff. VAT that can be reclaimed is called ‘input VAT’.

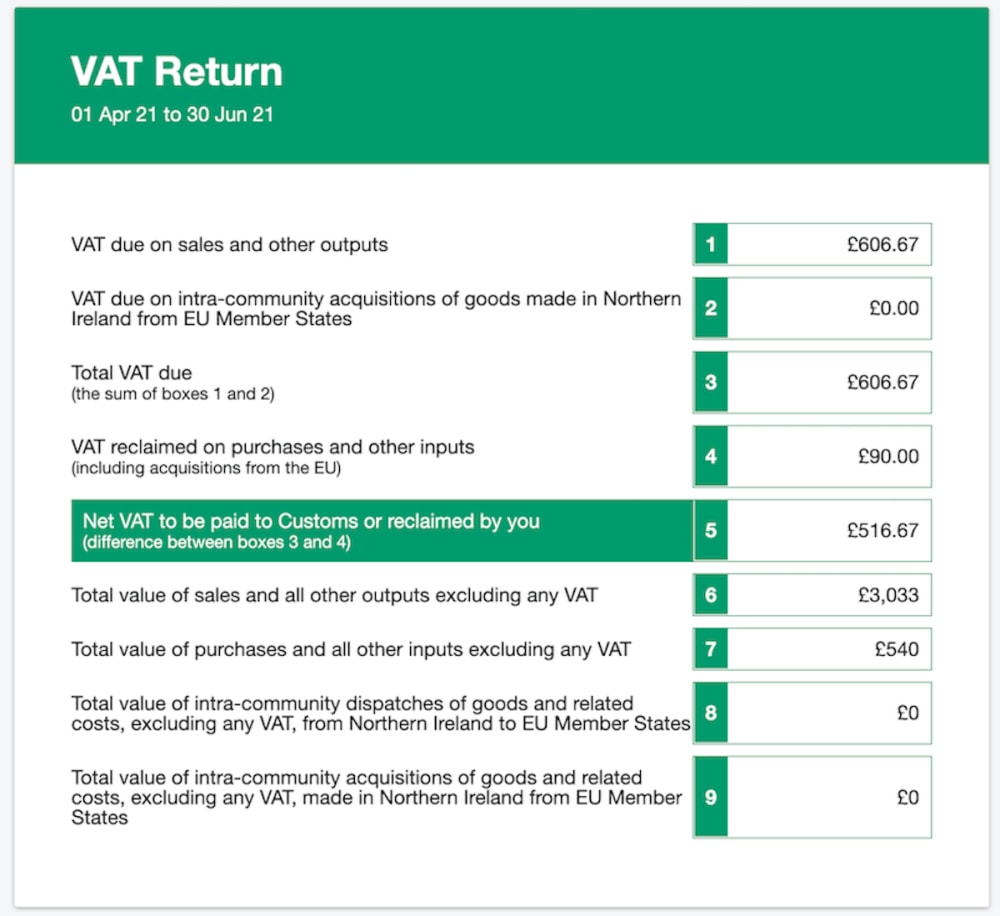

In order to declare how much output VAT you’ve charged and input VAT you’ve reclaimed, you must file a regular VAT return to HMRC. Your VAT return shows your business’s output VAT minus its input VAT - and the difference is what you must pay to HMRC.

If your input VAT is greater than your output VAT, you’ll get a refund from HMRC.

Filing your VAT return using FreeAgent

FreeAgent generates Making Tax Digital-compatible VAT returns automatically based on the accounting data you enter each quarter. When your VAT return is due, you can file it directly to HMRC from the software.

Find out more about VAT in FreeAgent

Managing the transition period

You apply to be registered for VAT as from a certain date, so there will usually be an interim period between that date and the arrival of your certificate and VAT registration number. You’ll have to charge output VAT on any sales after your registration date – but until your VAT registration number arrives, you won’t be able to issue official VAT invoices. In the interim period you’ll need to add the relevant rate of VAT - usually 20% - to the total value of all your invoices as from the date from which you’ve applied to be registered.

Once your VAT registration number comes through, you’ll need to re-issue any invoices that you issued to your customers during the interim period. This is so that your customers have official VAT invoices and can reclaim input VAT on the goods or services they’ve bought from you,

Remember that VAT can be exceptionally confusing, so if you have any queries about VAT and how it affects your business, you should check with HMRC or speak to an accountant for more advice.

Disclaimer: The content included in this guide is based on our understanding of tax law at the time of publication. It may be subject to change and may not be applicable to your circumstances, so should not be relied upon. You are responsible for complying with tax law and should seek independent advice if you require further information about the content included in this guide. If you don't have an accountant, take a look at our directory to find a FreeAgent Practice Partner based in your local area.

13th September 2024